Find UK property investment guides and videos that will help you work out what is a high yield on rental properties and which sectors offer the best high yield property investment returns for your property portfolio.

There are a range of different types of property investments available in the UK, but how can you choose the best types of investment properties for you?

From discovering where you can achieve the best UK rental yields to the prime areas for growth, our guides will enlighten you on the world of property depending on your investment requirements.

Our guides help you learn the fundamentals and discern the benefits of each class. Arm youself with relevant information; you are one click away from making a smart decision. If you'd like to conduct further research, try reading our UK property investment tips guide after this.

One Touch property consultants will share investment opportunities and guides with you to help you make an investment decision with confidence and ease.

High yield property investment UK with best returns

What high yield property investment UK can offer best returns?

There are no investment property guildelines into what makes a good return on rental property. The best returns on investment in UK property can be found in the care home and student property sectors. These are investments with a low vacancy rate.

Investors in the UK and EU who are thinking of keeping their money in a savings account will be hard-pressed to find banks offering more than 2.5% interest according to the latest figures from moneysupermarket.com. Obviously, this will be a disappointing return for those who have worked hard all their lives and want to build a nice retirement fund.

If you are fed up of getting low interest on your savings and are wondering how to increase achieve a high yield, we present a range of investment options, hopefully one of these appeal to you...

When we talk about a property yield, we mean the annual return likely to made on a property investment. A rental yield is calculated by taking the annual rental income and dividing it by the property value, and then multiplying by 100. This will give a gross yield percentage. To get a net yield percentage, factor in fees such as ground rent or a service charge.

What is a good yield on a rental property?

Typically, buy-to-let investments offer lower rental yields compared to commercial properties. This is due to a number of factors including the property price and tenancy type. There is a possibility to regularly review rental prices with property tailored towards short-term tenants, and property rented as serviced accommodation is typically more expensive than a regular residential property.

For investors who are looking to invest in buy-to-let property, a yield of around 5-8% is considered good. To find out where these rental yields are still possible for residential property, read our UK property hotspots guide.

Low interest environment allows landlords to take our mortgages and still attain good rental yields

In July, gross mortgage lending in Britain was up 9% year-on-year according to UK Finance. The number of approvals has also increased from 75,105 in June to 77,786 in July. Mortgage interest rates have also been slashed to entice the smaller buy-to-let market, with the Post Office being the latest lender to introduce a two-year fixed rate of 1.33pc, its lowest ever according to mortgage comparison site, Moneyfacts. These low interest rates allow investors to achieve a good yield on property investment as the cost of repaying the mortgage is lower and this is offset by rental income.

Older investors may already own their own home outright. According to Census data from 2011, three quarters of those aged 65 and over own their own home, 72% of which are either three bedrooms or more. Some of these owner-occupiers may be looking for retirement income to supplement their pension and ensure a more comfortable life, and may be eager to downsize to a more manageable property. With the additional equity that can be released individuals may consider investing in more property. Bearing that option in mind, what are some high yield investment options?

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Retirement property investments – high yielding property in a hands-off environment

Care home investments and later living retirement villages offer high yearly returns of more than 8%, for a guaranteed number of years. These are ideal for overseas investors who cannot afford the time to perform general maintenance tasks associated with more traditional buy to let properties as they are operated by a management company. The process involves the investor buying a room in an operating care home, and then leasing it back to the management company for a monthly return.

Residential care homes can generally achieve slightly higher yields if they accommodate self-funded residents. Sought-after care homes that provide assisted living services such as personal shopping, preapring meals and offering beauty treatments and entertainment are often luxurious, and individuals choose to stay there do so for the social experiences and community feel, not because they require nursing care.

These types of homes are in desirable retirement spots, such as the south west by the coast or the Isle of Wight. These areas are typically attractive to retirees, as they offer a temperate climate, idyllic countryside and a slower pace of life.

How good are student property investments UK?

It is understandable that with Brexit and the fall in the number of EU students applying for places at UK universities, investors perhaps have disregarded student property investments. Student accommodation investments can still generate a good rental yield if a prudent approach is taken and a city is chosen where there is still a significant student population.

Some cities have high percentages of EU students, and the appeal of prestigious universities such as Oxford or Cambridge will not wane, regardless of whether students have to pay higher tuition fees. Likely, this would be at the expense of other universities that are popular with EU students, such as Coventry (8.1% EU students) and Bath, (7.2% EU students) according to a recent report by KPMG.

Where can the best UK student accommodation investment be found?.

Investors can instead choose universities with a lower percentage of EU students, such as Sheffield (2.9% EU students). These universities will be less impacted by the fall in EU application numbers, and therefore accommodation in the city will not experience gaps in occupation due to a shortage of students.

Nebula is one such student property investment in S1 Sheffield. It is close to both the University of Sheffield and Sheffield Hallam University. Furthermore, Sheffield’s major attractions, pubs and shopping facilities are just a short walk or tram ride away which allows students to experience the very essence of the city. Each room boasts an en-suite bathroom, and according to Knight Frank, students are persuaded to spend over £160 per week on their accommodation if it offers these sorts of premium features. Units in Nebula can be purchased from £59,950 and the developer is offering a net yield of 9% which is contracted with the developer for three years. This shows that they are so confident that the units will be popular with students.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

The fall in the value of the pound – the rise in the number of tourists?

Perhaps a previously unconsidered benefit of Brexit and the subsequent fall in the value of the pound; Britain is now a more attractive destination for tourists. It isn’t just London that tourists flock to either, Liverpool has a particularly booming tourism industry. Home to The Beatles, Liverpool F.C., Everton F.C., the Albert Dock, Tate Liverpool and a host of other museums. It also has a large port, and thousands of people stop off at Liverpool to explore the city before continuing their onward journey.

Property: a stable investment option?

As we have previously mentioned, banks offer disappointing interest rates that would not serve someone wishing to grow their capital well. Blue chip defensive stocks also offer meagre returns, and some other investment options that offer higher returns carry with them a significant amount of risk such as Land Banking.

Investing in property in the UK has always been a popular option, due to the stability in the market. Despite additional rules and regulations being introduced (such as additional stamp duty charges), it remains a profitable market to invest in.

Investors who have concerns with how stamp duty increase can affect the profitability of their property can consider commercial investments such as student property and retirement home investments. These properties are exempt from stamp duty if the price does not exceed £150,000, making them a great option for people wanting to achieve strong rental yields because their purchase costs are lowwer. Even buy-to-let properties have reduced stamp duty until March 2021. Start searching for properties to invest in, to take advatage of the tax svaings before it is too late.

One Touch experienced investment consultants help individuals to find suitable high yield investment options that will allow them to achieve their financial goals.Contact us to discuss your requirements and available projects today.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

What is a freehold property?

What is a freehold property? How does it differ from a leasehold?

When buying property, freehold and leasehold are just two terms you will come across. It is vital you know the difference between a freehold property and a leasehold property, so what sets them apart?

Click on the green arrow to reveal the key differences =>

When buying property in England and Wales, you will come across the terms freehold and leasehold. The two terms describe the different ways you can own a property and generally apply to different property types. Note in Scotland and Northern Ireland slightly different rules apply.

What is a freehold property?

A freehold generally means outright owning the land and the dwelling that sits on it. Most houses in England and Wales are owned on a freehold basis.

A freehold property is sometimes seen as more desirable and thus more expensive due to the owner having absolute control of the property and land.

What is a leasehold property?

A Leasehold title refers to tenure. You are leasing the property, you own it and receive the title deeds for your property. However, you do not own the land on which it sits. It could be the case that someone who owns the freehold of the land grants a leasehold title which set about the length and annual ground rent.

Historically, these were 99 years, although the typical lease nowadays is for 125, with some leases being a long as 250 or even 999 years.

If this is the case, the lease will be lengthy, and an agreement will be drafted based on property and contractual law between the freehold owner (Lessor) and the tenant (Lessee). The leaseholder usually pays an annual fee called ground rent typically between £50 – £250.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Most flats are owned on a leasehold basis. Leases can easily be renewed and the freeholder has no way of denying the extension.

The length of the lease generally only impacts the properties price when there is less than 80 years on remaining. The good news is that a lease can easily be extended and the cost thereof determined by the by valuers using a standard formula. The UK government funded, Leasehold advisory service is there is assist leaseholders with any disputed with the freeholder.

In general, leaseholds are preferred by oversea investors because it is the freeholder’s responsibility to maintain the communal areas.

Service charge

The freeholder appoints a management company to take care of the structural integrity of the building and the common areas. They would also arrange building insurance and other aspects relating to the building and its exterior.

If the company is not doing a good job, under the terms of the Landlord and Tenant Act 1985 and 1987, the leaseholder can obtain the Right To Manage and appoint their own management company.

Conclusion

Leasehold is not bad. In Layman’s terms you own your apartment for which you obtain the title deeds. The freeholder owns the ground and receives an annual ground rent. The freeholder appoints an independent management company to provide maintenance and upkeep the communal areas for which the leaseholder pays an annual service charge. It means that owners only need to be responsible for the upkeep of their own property, which if you find the right tenant, is also taken care of.

At One Touch, we offer new build flats in modern developments mainly on a leasehold basis. We would love to assist you further on your property search so contact One Touch Property today to find out more about our range of buy to let property investments.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Property Investment Terminology UK Explained

Property Investment Terminology UK Explained

Investing in property can be daunting enough, without adding unique terminology to the mix. You want to be confident in your investment and familiar with all the terms used in documents.

Here, we explain all property investment terminology, acronyms, and abbreviations which will help you make informed decisions when it comes to a future investment. Click on the green arrow to discover the meaning of commonly used property jargon =>

Property Investment Glossary

If you are taking that first step into property investment, you may not be familiar with the terminology used. Whilst many terms are used in regular house buying, some terms and abbreviations can be completely new that first time investors may be unfamiliar with. To allow you to feel more comfortable reading through investment documents and brochures, we have broken down some of the most common property investment terminologies, and what they mean.

Below Market Value

Properties offered below the prices of what comparable properties in the area have sold at.

Buy to let investments

This is where you would buy a residential property and let it out, usually to professionals. Rental yields are usually lower to what can be achieved through a commercial property, but there is more scope for capital growth. Unless a management company is in place, you would be responsible for maintenance of the property including repairs and tenancies.

Capital Growth

The amount a property increases in value. Some properties have the potential to achieve more capital growth than others. Influencing factors can be the scale of regeneration in the area, improving transport links and job opportunities, and overflow from people priced out of surrounding areas.

Care Home investments

Invest in a room in a care home. A care home operator typically takes a 25-year lease with the care home investor. The company essentially runs their business from the premises leased from the owner. All day-to-day running of a whole care home business is completely taken care of and you would receive a guaranteed rental yield under a commercial contract. These are hands-off investments and demand is underpinned by Britain’s ageing population. These are usually cash only investments.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Commercial Property Investment

Commercial property generally refers to property that is used for business purposes. However, the term also extends to larger residential developments, such as student, care homes and hotels. There are five categories of commercial property and they are: offices, retail units, industrial, leisure and healthcare.

Council Tax

Local taxation in England, Scotland, and Wales on domestic property. In general, the occupier is responsible for payment of council tax, unless the property is an HMO in which case the landlord is responsible. Students are exempt from council tax and it is not applicable to care homes which means higher returns can be achieved.

Crowdfunding

Funding from a large group of people which is usually done online. For example, 100 or so people could club together to buy a property and receive a share of the rental yields and capital growth.

Diversification

The art of investing in a variety of assets to minimise exposure to market volatility.

Freehold

Owning the property and the land it sits on.

Gross Rental Yield

The amount of money a landlord or investor makes on a property before costs relating to the property (.e.g mortgage) have been deducted. Usually presented in a percentage figure.

Ground Rent

An annual charge the leaseholder pays to the freeholder for the ground the

property sits on.

High Net Worth Investor

In the UK, a high net worth investor is defined as someone who has an annual income of £100,000 or more or has net assets to the value of £250,000 or more.

HMO

House in multiple occupation. A property that is rented out to three or more people who are not family and are not part of one household but share the house’s facilities such as the kitchen and bathroom. It is otherwise known as “house share” or “flat share”.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

HMO Licence

If a landlord wants to rent a property as an HMO in England or Wales, they would need to check whether they need an HMO Licence. This is a must if the house is occupied by five or more people and at least one tenant pays rent.

A licence is valid for a maximum of five years and costs £1,100. The purpose of the licence is to ensure the house is fit for purpose. The council requires landlords to submit electrical safety certificates and gas safety certificates and install fire alarms in the property. Of course, it is an extra cost and we have found many people have started to move away from buy to let and consider other property investments that are not subject to the same licensing.

HMRC

Her Majesty's Revenue and Customs is a government department tasked with collecting taxes and other payments such as National Insurance.

Hotel room investments

These are categorised under commercial property investments. Investors would usually purchase a hotel room which is then leased back to the management company under a commercial contract. Investors would usually receive fixed yields for a defined period. There would be various clauses in the contract that would allow the company to buy back the hotel room from the investor at an increased price. This is usually after five years +. Hotel room investments are usually hands-off and sometimes a complimentary two-week stay per year is offered.

Leasehold

Leasehold is the customary form of ownership used for apartments. The freeholder grants a lease typically between 125 and 250 years to the leaseholder. The land itself belongs to the freeholder. The Leaseholder owns the apartment. The freeholder cannot withhold granting a lease extension. There is standard calculation of the lease extension which a chartered surveyor will provide according to the Government set parameters. Generally the freeholder would be responsible for maintaining the building.

Loan to Value Ratio - LTV

The ratio of a loan to the value of the property. For example, if your property costs £100,000 and you take out an £80,000 loan on it, that would be an 80% loan to value.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

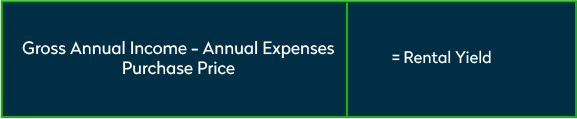

Net Rental Yield

The net rental yield is the amount of money an investor makes on the property through rent once all the payments in relation to the property (e.g. mortgage) have been deducted. It is presented as a percentage figure, calculated by taking the yearly rental income of a property and dividing it by the property price. Investors should compare rental yields achieved from similar properties in the area to understand the potential. The formula is as follows:

NRL1

A form to be completed by a non-resident landlord. If a landlord usually resides outside of the UK they can complete an NRL1 form to ensure the income they make in the UK is not taxed in the UK. The income may be subject to tax in the landlord’s home country.

Off Plan

To buy off-plan means to purchase a property prior to its completion. Investment property that is off plan tends to have payment plans in place where investors can pay in installments. This may make investment more manageable for someone who does not have the full capital at the present time.

PBSA

Purpose-built student accommodation. Housing built for students by private developers. Generally, these are either collections of self-contained studios with shared living spaces, or traditional halls of residence with en-suite bedrooms and shared kitchens.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Personal Allowance

The amount you can earn in the UK that you do not have to pay day on. It can change from year-to-year, but in the 2020/21 tax year it is £12,500.

Portfolio

If an investor owns several properties, it is referred to as a portfolio.

Purchase Process

The process of purchasing a property. With an investment property this would usually involve, choosing a property within a specific sector, paying a reservation deposit, instructing solicitors, exchanging contracts, stage payments until completion and then upon completion finding a tenant and collecting rent.

Instructing a solicitor to undertake the conveyancing process usually costs between £900+Vat - £1250+Vat

Return on investment

A return on investment is defined as the ratio of profit divided by the total cost of the investment.

Service Charge

A charge imposed on the leaseholder by the freeholder to maintain the property and carry out basic repairs. This may include heating and lighting in communal areas, upkeep of communal gardens and lift maintenance.

Stamp Duty

Stamp duty is paid in the UK if someone buys a house, flat, land or buildings over a set price. It is not applicable to first time buyers whose purchase is under £300,000. Stamp duty is 5% for first time buyers whose home is priced between £300,001 to £500,000.

Property or lease premium or transfer value SDLT rate

Up to £125,000 Zero

The next £125,000 (the portion from £125,001 to £250,000) 2%

The next £675,000 (the portion from £250,001 to £925,000) 5%

The next £575,000 (the portion from £925,001 to £1.5 million) 10%

The remaining amount (the portion above £1.5 million) 12%

If you already own a property and you are buying another one, you will have to pay an additional 3% on top of the standard stamp duty rate.

Student property investments

These are often in the form of student HMOs or purpose-built student accommodation. Student HMOs are residential properties that have been repurposed to accommodate students. Each student will have their own bedroom but will share other facilities such as a kitchen or bathroom with other students. There are some benefits to owning this type of property. If an investor chooses to sell, it can be sold on to a residential buyer who wishes to make it their own home or a buy to let. This means there is more scope for capital growth as there is a larger market to sell to.

If an investor chooses to buy a student HMO, they will be expected to maintain it. This means that they would have to organise new tenancies and undertake any repairs. If they choose to buy a cheaper property to maximise rental yields, they would have to be mindful of how much they’d need to spend to bring it up to standard.

Purpose-built student accommodation is developed especially for students. It’s often newer with more high-spec facilities. The development is maintained by a management company, so investors do not have to worry about sorting out repairs or new tenancies. They also would not have to account for gaps in occupancy as this is absorbed by the management company. Investors would have to pay a yearly fee to the management company though, and units cannot be repurposed for residential use, so the market is more limited.

Armed with an understanding of these terms, you will be better equipped to explore different property investments. If you want to invest in buy to let, we recommend reading our best places to invest guide, if you want to invest in student property, why not read our checklist to successfully invest in student property.

The UK Property Purchase Process

The UK Property Purchase Process Explained

If you are considering buying UK residential property as an investment. Before you decide to invest, read our explanation of the UK property purchase process. It will set your mind at ease.

If you are looking for tips for investing in UK property, you might benefit from having a free consultation for one of our experienced investment consultants to get a clear idea of what you are hoping to achieve.

Are you looking to invest for the short term and achieve good levels of rental yields, or are you looking to hold on to your investment for a longer time for capital growth?

If you are looking for high rental yields – often a characteristic of alternative commercial property – you should consider investment classes such as student property and care home investments. Many Chinese agents are selling UK property but when it comes to alternative property classification it is recommended that your agent works with a specialist property broker such as Knight Frank or One Touch Property Investment. Our useful property investment guides and property investor news on a the buy-to-let, student and care markets are essential to make an informed investment decision.

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Work out your budget

The pound sterling is not faring well against other currencies so those overseas may be able to get a more favourable exchange rate. Commercial property such as student and retirement home investments are generally not mortgageable, but units have a lower entry point compared to buy to let. You would be able to get a mortgage on residential properties over £100,000. Interest rates would be 4% but the rental income generated through the property would be able to cover mortgage payments.

Ultimately, buying a property whether as a buy-to-let investment or otherwise is quicker if you are a cash buyer as you will not have to spend time filling in mortgage applications.

Do I have to visit the UK to purchase property?

People from overseas can invest in the UK, and you do not have to visit the UK to purchase property in the country. The legal side is handled by a solicitor and if you used a property investment company such as One Touch Property, they would be able to provide guidance on different investment types in different cities.

Of course, you may want to visit the city you eventually decide to invest in. Some people choose to invest in a certain city or area they feel an affinity with. They might enjoy the status of owning property in that area, like the location, or recognise the impact regeneration has on capital growth of property prices. It’s based on personal preference and the amount of importance one would place on an area.

The basic property purchase process

Once you have decided what your objectives are with the investment and have calculated how much money you have for it, you review each investment that is presented to you. If you find an investment you feel comfortable with, you would have to choose a unit and pay a reservation deposit usually between £2,000 – £5,000.

Next your agent will instruct solicitors on your behalf who will do all the legal work and carry out all the necessary legal checks. Once that is completed there would be an exchange of contract and at that point you would pay 50% of the property price minus the deposit. There would be another stage payment of 25% and then the balance would be payable upon completion.

After this you would receive your income. This will typically be paid quarterly. Overseas investors will need to complete a Nrl1 tax form. As the investments One Touch Property Investment offer are hands-off, investors will not have to worry about advertising for potential tenants or carrying out maintenance task.

The UK is an attractive place for home ownership, it’s seen as a politically stable and prosperous country. Liverpool was named the European Capital of Culture in 2008 and Manchester was ranked the 38th most liveable city in a global list that measures crime rates, access to healthcare and social stability. London is the jewel in the crown boasting a rich history and the financial capital of Europe.

As negotiations for Britain’s departure from the European Union are drawn out, the value of the pound has dipped against other currencies which has in turn made property more accessible to overseas investors. This makes it an ideal time to consider investing.

If you are unfamiliar with how property investment works within the United Kingdom, it may be helpful to get in contact a expert property investment consultants at One Touch to help you form a buy-to-let strategy and provide guidance on the most attractive sectors. Every aspect could be covered including presenting you with a range of suitable investment opportunities through to introducing property professionals such as solicitors and property management companies. If you're searching for properties overseas and looking at the UK, contact one of our experts today

Start your property journey...

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

All you need to know right here in one comprehensive buy to let guide. Inside you will learn the long term link between house prices and supply, deciphering the best places to invest and investment property returns.

UK Buy-To-Let Guide

By filling in your details you acknowledge that you will be joining our mailing list to receive property investment news and relevant property investments.

Call Back Request

Enter your details to request a FREE call back.

Please complete all fields

Call us on +44 20 4572 9663

By completing this form, you give us permission to send your contact information to the property developer or their appointed agent.

They are best positioned to answer your queries and will call you back to discuss your requirements and send you relevant information.

Videos

UK Property Sourcing Strategy

One Touch Property’s Investment Director Arran Kerkvliet explains our UK property sourcing strategy. Arran explains the due diligence checks One Touch carries out on each developer, to ensure that they are reputable and that each investment logistically stacks up.

We conduct site visits for previous projects to understand the quality of finish that we could expect.

After meeting the developer, we get in touch with our independent solicitors for them to review the proposed purchase agreement to establish if there is anything in the fine print that could be to our client’s detriment.

Q&A How Do I Sell My Student Property?

One Touch Property’s Stuart Cowie explains a bit about what One Touch Property do, the company ethos and how our investment consultants are dedicated to helping you achieve your financial goals by matching you up with the most suitable property investment opportunity.

One Touch Property are an award winning student property broker offering student property investments. We have been operating in the student market since 2011. We are your first choice in student property opportunities because we have with the widest range of U.K student accommodation investments to suit your requirements and preferences in areas of high demand such as Birmingham and Liverpool. The best performing investment rental property can be found right here. We help clients to acquire their first student buy-to-let investment as well as facilitating the resale of existing client’s properties. As our name suggests, One Touch Property make it easy from start to finish.

Want to see more?

Subcribe to our Youtube Channel for more insightful videos and guidance on property Investment